You opened your demat app in January. Green everywhere. Confidence sky-high.

By May, your portfolio looked like a Holi celebration gone wrong — red splattered all over. You stopped checking. You started doubting.

If that’s you, breathe. You are not alone, and you are not stupid. You just got a front-row seat to one of the wildest years D-Street has seen.

Here’s why this matters right now: the Indian stock market 2026 has been a brutal teacher. Sensex slipped from around 83,000 in January to the mid-74,000s by June. Foreign investors yanked out over ₹2 lakh crore. And yet — and this is the part nobody texts you about on the family WhatsApp group — quiet, boring, disciplined investors are still building real wealth. Let’s talk like a smart older sibling would, over chai, without the jargon and without the hype.

What’s Actually Happening in the Indian Stock Market 2026

Let’s start with the truth, not the headlines.

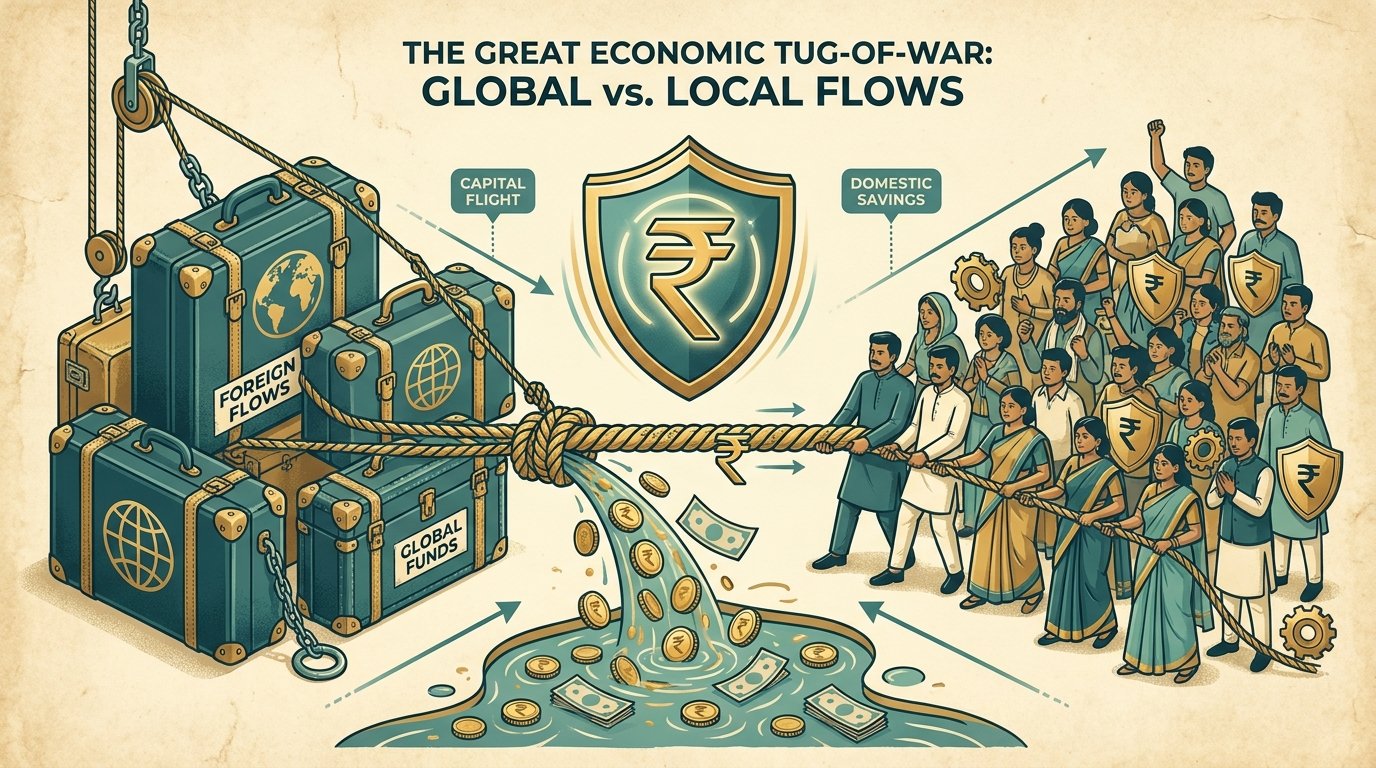

After two roaring years, the market hit a wall. Foreign Institutional Investors (FIIs) — the big global funds — turned into relentless sellers. In just the first few months of 2026, they offloaded more Indian equities than they did in all of 2025. That’s not a typo. One year’s worth of selling, squeezed into a few months.

The result? Sharp, stomach-churning drops around key Nifty levels. Some days the index would fall 1.5% before lunch. Your ₹1 lakh felt like ₹88,000 by evening.

Corrections feel like the end of the world. They’re actually just the market clearing its throat after a long, loud speech.

But here’s the nuance the panic-mongers skip: the market corrected, it did not collapse. There’s a big difference, and understanding it is the first step to investing like an adult.

Why Did the Market Fall? The Real Reasons (Not the WhatsApp Version)

Your uncle will tell you “foreigners are running away from India.” Half-true. Lazy. Here’s the fuller picture.

Several things piled up at the same time:

- US bond yields rose. When American government bonds pay more, global money flows back to the safety of the US dollar. India looks less juicy by comparison.

- The rupee weakened. It touched record lows near ₹96–97 per US dollar. A falling rupee quietly eats into foreign investor returns, so they sell faster.

- Crude oil spiked. Middle East tensions pushed oil prices up. India imports most of its oil, so this hits inflation, the rupee, and corporate margins all at once.

- Earnings were soft. Several quarters of underwhelming company profits made stretched valuations look expensive.

- Growth cooled. GDP growth estimates were trimmed. Some global brokerages even whispered the scary word — “stagflation.”

No single villain. A whole ensemble cast. That’s almost always how corrections work — many small pressures arriving together, not one dramatic crash.

The Plot Twist: Why India Didn’t Crater

This is the most beautiful, under-reported story of 2026.

While FIIs were busy selling, somebody was buying every single share they dumped. That somebody was us. Domestic Institutional Investors (DIIs) — Indian mutual funds, insurance companies, pension funds — pumped in over ₹3 lakh crore, soaking up the foreign exit.

And where did that DII money come from? From your monthly SIP. From crores of salaried Indians auto-debiting ₹500, ₹2,000, ₹10,000 every month into mutual funds, rain or shine, Sensex up or down.

This is a genuine structural shift. A decade ago, when FIIs sneezed, India caught pneumonia. In 2026, the SIP army acted like a giant shock absorber. The market became more internally driven — funded by Indian savings, not foreign moods.

Read that again, because it changes everything: the most powerful force holding up the Indian stock market 2026 is ordinary people quietly investing every month. People exactly like you.

Sensex, Nifty and What Analysts Actually Predict for 2026

Let’s address the question burning in your mind: where does it go from here?

Nobody knows for certain — and anyone who promises a precise number is selling something. But here’s the broad consensus floating around major brokerages and research desks in 2026:

| Source / View | Outlook for 2026 | What It Means for You |

|---|---|---|

| Bullish brokerages | Nifty heading toward ~29,000 by year-end if earnings recover | Meaningful upside for patient large-cap investors |

| Cautious-optimist view | Recovery building in the second half of 2026 as rate cuts kick in | The pain is likely front-loaded; back-half could be kinder |

| Bearish risk case | More volatility if oil stays high and the rupee stays weak | Don’t bet money you’ll need within 2–3 years |

The honest summary? Valuations cooled to near their long-term averages, earnings are expected to grow at a healthy clip over the year, and FII selling tends to reverse eventually. Many analysts believe the worst of the fall is behind us — but “believe” is not “guarantee.”

Your job isn’t to predict the bottom. It’s to keep investing through the uncertainty.

How to Actually Invest in This Market (Without Losing Sleep)

Theory is nice. Let’s get practical.

Meet Ravi, a 28-year-old software engineer in Bengaluru earning ₹80,000 a month. In January he saw friends posting screenshots of small-cap gains and dumped ₹2 lakh of savings into three “hot tips.” By May, that ₹2 lakh was ₹1.3 lakh. He panic-sold and swore off stocks forever.

Now meet Priya, a 31-year-old marketing manager in Pune earning ₹55,000. She did something boring: a ₹15,000 monthly SIP split across a Nifty index fund and a flexi-cap fund. When markets fell, her SIP bought more units at lower prices. She didn’t check her portfolio daily. By June, she was calmly accumulating, completely unbothered.

- Investing in US Stocks? 8 Things to Learn Before You Start Thinking about investing in US stocks but not sure where to begin? Here are the 8…

- What Actually Happens When You Click ‘Buy’ on a Stock When you tap Buy, your order races through four institutions and matches with a stranger in…

- What is a Share/Stock? A Simple Explanation If you’ve ever wondered “What is a Share/Stock?”, you’re not ... Read more

- What is the Stock Market? If you have ever tried to understand the stock market, ... Read more

Same market. Two completely different outcomes. The difference wasn’t intelligence — it was process.

Here’s the grown-up playbook:

- Decide your time horizon first. Money you need in under 3 years has no business in equity. Park that in an FD, RD, or liquid fund.

- Default to SIPs, not lump sums. Rupee-cost averaging is your superpower in a volatile year. Volatility becomes your friend, not your enemy.

- Start with index funds. A simple Nifty 50 or Nifty 500 index fund gives you instant diversification at rock-bottom cost. Boring beats clever for most people.

- Get your asset allocation right. A rough rule: equity percentage ≈ 100 minus your age. A 30-year-old can comfortably sit at 70% equity, 30% debt.

- Use the tax breaks. ELSS funds give equity exposure plus a deduction under Section 80C. PPF and EPF anchor your safe portion.

That’s it. No tips. No timing. No drama.

Sectors and Themes Worth Watching in 2026

If you do want to go beyond index funds, focus on themes with real legs — not whatever is trending on Telegram.

- Financials and banking: Beaten down during the FII exit, but the backbone of a growing economy. Quality private banks often lead recoveries.

- Domestic consumption: A young, spending India keeps powering FMCG, retail, and consumer brands through cycles.

- Infrastructure and capex: Government spending, PLI schemes, and a manufacturing push support engineering, power, and PSU names.

- Energy: Surprisingly resilient when oil is high — a natural hedge inside a portfolio.

One caution: themes rotate fast. The leader of one quarter is often the laggard of the next. This is exactly why a diversified fund usually beats your sector-picking instincts. Be humble.

Quick honesty note: none of this is personalised financial advice. Your situation, goals, and risk appetite are unique — treat this as education, not instructions.

Things Nobody Tells You (The Mistakes That Quietly Drain Wealth)

Most people don’t lose money in the market because of the market. They lose it because of themselves. Watch for these:

- Stopping your SIP during a fall. This is the single most expensive mistake. You’re literally cancelling your discount sale.

- Checking your portfolio daily. Daily checking turns long-term investors into nervous traders. Once a month is plenty.

- Chasing last year’s top performer. The fund that topped the charts rarely repeats. You buy high, then watch it cool.

- Confusing trading with investing. Intraday trading is a full-time, high-skill, high-loss game. SIP investing is a marathon you can run in your sleep.

- Ignoring an emergency fund. Without 6 months of expenses parked safely, one job loss forces you to sell stocks at the worst possible time.

- Listening to free tips. If a stock tip is free and forwarded on WhatsApp, you are the product, not the beneficiary.

- Forgetting taxes. Selling within a year triggers higher short-term capital gains tax. Holding longer is often rewarded — patience even saves you money.

Avoid these seven, and you’ll already be ahead of the majority of retail investors in India.

Your 7-Day Action Plan for the Indian Stock Market 2026

Enough reading. Here’s exactly what to do this week, one step at a time.

- Day 1 — Build your safety net. Confirm you have at least 3–6 months of expenses in an FD or liquid fund. No emergency fund, no stocks. Period.

- Day 2 — Open or clean up your demat. If you don’t have a demat account, open one with a SEBI-registered broker. KYC takes minutes via UPI and Aadhaar.

- Day 3 — Decide your monthly number. Pick a SIP amount you can sustain for years even on a bad month — say ₹2,000, ₹5,000, or 15% of your salary.

- Day 4 — Choose simple funds. Start with one Nifty index fund and one flexi-cap fund. Add an ELSS fund if you need 80C tax savings.

- Day 5 — Automate the SIP. Set the auto-debit for the day after your salary lands. Make investing a default, not a decision.

- Day 6 — Write your rules. On paper: “I will not stop my SIP when markets fall. I will check my portfolio once a month.” Sign it.

- Day 7 — Switch off the noise. Mute the panic WhatsApp groups. Unfollow the doom-scrolling finance accounts. Boredom is a strategy.

Do this and you’ve built a wealth machine that runs whether the Sensex is screaming up or sulking down.

Frequently Asked Questions

Is 2026 a good time to start investing in the Indian stock market?

Honestly, yes — for long-term investors, a corrected market is often a gift, not a threat. Valuations cooled toward their long-term averages in 2026, meaning you’re buying at saner prices than at the January peak. Just commit to a 5–7 year horizon and invest via SIP rather than timing the bottom.

Will the Sensex and Nifty recover in 2026?

Many analysts expect recovery to strengthen in the second half of 2026 as earnings improve and interest rates ease, with some bullish targets placing Nifty meaningfully higher by year-end. But forecasts are educated guesses, not promises. Invest based on your goals and time horizon, not on any single prediction.

Why are foreign investors (FIIs) selling Indian stocks?

Mainly global reasons, not Indian weakness: higher US bond yields, a stronger dollar, costlier crude oil, and a weaker rupee made foreign investors trim their India exposure. Importantly, Indian domestic investors absorbed most of that selling, which is why the market corrected without crashing.

Should I stop my SIP because the market is falling?

No — this is the most damaging mistake retail investors make. When the market falls, your fixed SIP amount buys more units at lower prices, lowering your average cost. Stopping a SIP during a dip is like walking out of a sale just as prices drop. If anything, keep it running.

How much money do I need to start investing in stocks in India?

Less than a pizza. You can start a mutual fund SIP with as little as ₹100–₹500 a month, and buy individual shares for whatever a single share costs. The amount matters far less than consistency. Starting small and staying regular beats waiting to invest a big lump sum “someday.”

Are index funds better than picking individual stocks in 2026?

For most people, yes. Index funds give you the whole market cheaply, remove the stress of stock-picking, and quietly beat the majority of active investors over the long run. Pick individual stocks only with money you can afford to lose and time you’re willing to spend researching.

The Bottom Line: Boring Wins

The Indian stock market 2026 handed out a masterclass in fear. Red screens, scary headlines, FIIs heading for the exit. And through all of it, the quiet investors — the ones running their SIPs, ignoring the noise, thinking in years — kept building wealth one boring month at a time.

You don’t need to be a genius. You don’t need a hot tip. You need a plan, a little patience, and the discipline to not panic-sell when your group chat does.

Markets will fall again. They always do. They’ll also rise again — they always have. Your edge isn’t predicting which day. It’s simply staying in the game long enough for compounding to do the heavy lifting.

Start your SIP this week. Keep it simple. Stay boring. Future-you, sitting on a portfolio you barely had to think about, will quietly thank present-you. Ready to go deeper? Explore our guides on starting your first SIP and choosing the right index fund on IndiFinance — and turn this year’s chaos into your decade’s biggest opportunity.