You open a brokerage app on a slow Sunday, finally ready to start saving for retirement. You pick ‘IRA.’ And then the app asks one innocent-looking question: Roth or Traditional?

You shrug. You pick one. You move on.

Here’s the uncomfortable truth: that five-second decision can quietly add — or quietly cost you — six figures by the time you retire. Same money going in. Wildly different money coming out.

If you’re an Indian professional building a life in the US — on an H-1B, a green card, or a fresh passport — retirement accounts probably feel like the boring, ‘deal-with-it-later’ corner of your money. But 2026 just made this choice more interesting. Contribution limits went up. Income rules shifted. And one new rule now quietly nudges some high earners toward Roth whether they like it or not.

So let’s settle the Roth vs Traditional IRA debate properly — no jargon, no lectures, no preaching. Just the stuff that actually changes your bank balance.

So… what even is an IRA?

Think of an IRA — an Individual Retirement Account — as the American cousin of India’s PPF or NPS. It’s a personal retirement pot the government rewards you for using, as long as you mostly leave it alone until you’re older.

The ‘individual’ part matters. This isn’t your employer’s 401(k). You open it yourself, you fund it yourself, and you choose what it holds — index funds, ETFs, individual stocks, whatever you like.

And inside that pot, your money grows without the yearly drag of capital-gains tax nibbling away at every dividend and gain. That tax shelter is the whole point of the account.

The only real fork in the road is one simple thing: when you pay your taxes. Which brings us to the question that decides everything.

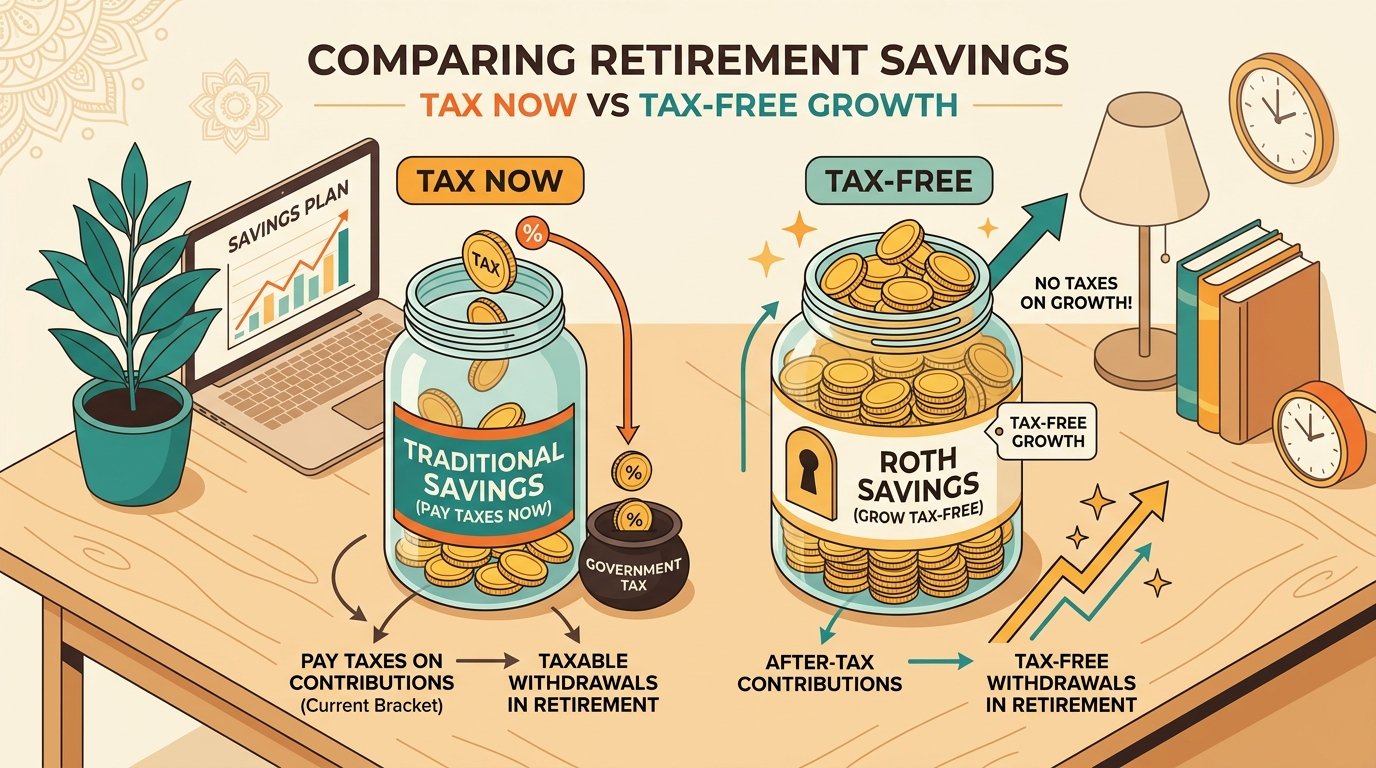

Roth vs Traditional IRA: the one difference that changes everything

Strip away all the noise and the entire choice comes down to a single word: when.

Traditional IRA: you (often) get a tax deduction today. Your money grows untaxed for decades. Then you pay ordinary income tax on every dollar you withdraw in retirement. Tax break now, tax bill later.

Roth IRA: no deduction today — you fund it with money you’ve already paid tax on. But it grows tax-free, and every qualified dollar you pull out in retirement is 100% tax-free. Pay the tax once, now, and never again.

That’s genuinely it. Everything else is detail. Here’s the side-by-side:

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| When you get the tax break | Usually upfront (a deduction) | Later (tax-free withdrawals) |

| How it grows | Tax-deferred | Tax-free |

| Withdrawals in retirement | Taxed as ordinary income | Completely tax-free |

| Income limit to contribute | None (deduction may phase out) | Yes (phases out at higher income) |

| Required withdrawals (RMDs) | Yes, starting at age 73 | None, ever, in your lifetime |

| Pulling out money early | Penalty before 59½ | Your contributions anytime, penalty-free |

Read that last row twice. It’s a quiet superpower we’ll come back to.

The 2026 numbers you actually need to know

These rules shift every year, so let’s anchor on 2026 — the figures that apply right now.

For 2026, you can put up to $7,500 across all your IRAs combined. If you’re 50 or older, you get a catch-up and can contribute $8,600. Both numbers ticked up from 2025.

Here’s the catch most beginners miss: that’s a combined limit. You don’t get $7,500 for a Roth and another $7,500 for a Traditional. Split it however you like — say $4,000 to Roth and $3,500 to Traditional — but the total tops out at $7,500.

Now the bigger trap: Roth IRAs have income limits. Traditional IRAs don’t. If you earn above a certain amount, the front door to a direct Roth contribution simply closes.

| Filing status (2026) | Full Roth contribution if your income is… | No Roth allowed once you cross… |

|---|---|---|

| Single / Head of household | Below $153,000 | $168,000 |

| Married filing jointly | Below $242,000 | $252,000 |

Between those two numbers, the amount you’re allowed to put in a Roth shrinks on a sliding scale. Above the top number, the front door shuts — but stay with me, there’s a side door coming.

Anyone with earned income can contribute to a Traditional IRA, no income ceiling. Whether you can deduct that contribution is a separate question that depends on your income and whether you (or your spouse) are covered by a workplace plan like a 401(k).

When a Traditional IRA is the smarter move

Meet Arjun. He’s 38, a senior product manager in New Jersey, earning a strong salary and sitting comfortably in a high tax bracket. For him, every dollar he can deduct today saves a meaningful chunk of tax this year.

For someone like Arjun, a Traditional IRA’s upfront deduction is genuinely valuable — if he qualifies for it. He’s making a quiet bet: that his tax rate in retirement will be lower than it is right now, at the peak of his earning years.

A Traditional IRA tends to win when:

- No Cosigner? No Problem: How International Students Actually Get US Student Loans No US relative to cosign your loan? Here's the real, lender-by-lender breakdown of how international students…

- The 401(k) Match: How Skipping ‘Free Money’ Quietly Costs You Six Figures One in four workers skip part of their 401(k) match — handing away a guaranteed return.…

- US Student Visa in 2026: What Every Indian Applicant Must Know Before Applying F-1 visa rejections for Indian students hit 61% in 2026. Learn how the India-US trade reset,…

- Stop Losing Money to Inflation: 5 Proven Ways to Protect Your Purchasing Power The Invisible Thief in Your Wallet Imagine waking up one ... Read more

- You’re in a high tax bracket today and expect a lower one in retirement.

- You want to shrink this year’s taxable income right now.

- You’re closer to retirement, so there are fewer years of tax-free growth to give up.

The honest catch: every withdrawal in retirement is taxed as income. And starting at age 73, the IRS forces you to begin taking Required Minimum Distributions (RMDs) — pulling money out and paying tax on it whether you actually need it or not.

When a Roth IRA quietly wins

Now meet Priya. She’s 28, a software engineer in Austin earning $95,000. Her tax bracket today is modest — and she has 35-plus years of compounding stretching out in front of her.

For Priya, paying a little tax now (while her rate is low) and then letting decades of growth come out completely tax-free is a beautiful deal. If her $7,500 quietly grows into $90,000 over the years, she keeps every single cent. No tax on the gains. Not now, not ever.

A Roth IRA tends to win when:

- You’re young or early in your career, with a long runway for tax-free compounding.

- You’re in a lower tax bracket now than you expect to be later.

- You value flexibility — you can pull out your contributions anytime, tax- and penalty-free.

- You’d rather not be forced to withdraw: Roth IRAs have no RMDs during your lifetime.

That flexibility is wildly underrated. Because you already paid tax on your Roth contributions, you can take those out in a real emergency without penalty — just leave the earnings alone to keep growing. It’s not a license to raid your future. But it’s a quiet safety net that India’s PPF lock-in never gives you.

The income trap (and the backdoor most people miss)

So what happens to high earners — say a dual-income couple in California clearing $300,000 — who get locked out of the Roth front door entirely?

They use the backdoor Roth. It sounds shady; it’s completely legal. You contribute to a Traditional IRA (which has no income limit), then convert that money into a Roth. The end result: Roth dollars, even on a high income.

It isn’t magic, and it has tax wrinkles — especially if you already hold pre-tax money in other IRAs, thanks to something called the ‘pro-rata rule.’ If your finances are even a little complex, this is the one spot genuinely worth a quick chat with a tax professional before you press the button.

One more 2026 wrinkle worth knowing: a new rule now requires people who earned more than $150,000 last year to make their workplace-plan catch-up contributions as Roth instead of pre-tax. The quiet era of mandatory Roth has officially begun.

Things nobody tells you about IRAs

The shiny brochures skip the messy parts. Here’s what actually trips real people up:

- The ‘I’ll decide later’ tax. Money parked in a savings account quietly loses to inflation while you ‘research.’ An imperfect IRA started today beats a perfect one started in three years.

- Opening is not the same as investing. Funding your IRA but leaving the cash sitting uninvested is shockingly common. The account is just an empty basket — you still have to buy the fruit (index funds, ETFs).

- The 5-year rule. For your Roth earnings to come out fully tax-free, the account generally has to be open for five years and you have to be at least 59½. Translation: open one early, even with a tiny amount, just to start the clock ticking.

- Forgetting the limit is combined. It’s $7,500 total across all your IRAs. Overshoot and the IRS charges a 6% penalty every single year until you fix it.

- Tax-bracket tunnel vision. Nobody truly knows what tax rates will look like in 30 years. That uncertainty is itself a quiet argument for owning a bit of both — call it tax diversification.

Your 7-day IRA action plan

Enough theory. Here’s how to go from ‘someday’ to actually done — this week:

- Day 1: Estimate your tax bracket this year. High and stable? Lean Traditional. Lower or early-career? Lean Roth.

- Day 2: Check your income against the 2026 Roth limits above to see whether the front door is even open for you.

- Day 3: Open an IRA at a low-cost provider (Fidelity, Schwab and Vanguard are the usual suspects). It takes about 15 minutes.

- Day 4: Set up an automatic transfer — even $200 a month. Automating beats willpower every single time.

- Day 5: Actually invest the money. A simple, low-cost total-market or S&P 500 index fund is a perfectly good starting point.

- Day 6: Turn on auto-contributions so next year quietly takes care of itself.

- Day 7: Write down your ‘why’ in one line. Future-you will read it on the days the market dips and panic whispers.

For the bigger picture, pair this with our guides on maximizing your 401(k) match and building an emergency fund first.

Frequently asked questions

Roth vs Traditional IRA — which is better for a beginner?

If you’re young and in a modest tax bracket, a Roth is usually the quiet long-term winner — you lock in today’s low tax rate and let decades of growth come out tax-free. If you’re a high earner who wants a deduction today, Traditional makes more sense. When in doubt, Roth is a hard choice to regret early in your career.

Can I have both a Roth and a Traditional IRA?

Yes, and many people do. Just remember the contribution limit is combined: in 2026, $7,500 total across both accounts ($8,600 if you’re 50 or older), not per account. Splitting your money between the two is a legitimate way to hedge against uncertain future tax rates.

What if I earn too much to contribute to a Roth IRA?

You’re not necessarily shut out. Many high earners use the ‘backdoor Roth’ — contributing to a Traditional IRA (no income limit) and then converting it to a Roth. It’s legal and common, but it has tax nuances, so it’s worth a quick word with a tax professional if you hold other pre-tax IRA money.

Can I withdraw money early without a penalty?

With a Roth, you can pull out your contributions (the money you put in) anytime, tax- and penalty-free — your earnings are a different story. With a Traditional IRA, withdrawals before 59½ generally trigger income tax plus a 10% penalty. So a Roth quietly doubles as a backup emergency cushion in a true pinch.

I’m in the US on a visa or green card — can I still open an IRA?

Generally yes, if you have US earned income, a Social Security number, and you file US taxes. Your visa status doesn’t automatically disqualify you. The bigger thing to plan for is what happens to the account if you eventually move back to India — that’s worth checking with a cross-border tax advisor before you go.

The bottom line

Here’s the reassuring thing about the Roth vs Traditional IRA decision: there’s rarely a truly ‘wrong’ answer. Both options beat doing nothing by a country mile. The real mistake is staring at the choice for years and never actually starting.

If you’re young and your tax rate is modest, Roth is usually the quiet long-term champion. If you’re a high earner hungry for a deduction today, Traditional earns its place. Not sure? Owning a little of both is a perfectly smart hedge against a future none of us can predict.

So pick one. Fund it. Invest it. Then let compounding do its unglamorous, life-changing work in the background. Future-you — sipping chai on a sunny porch somewhere, taxes already handled — will quietly thank you.

Ready to go deeper? Explore our beginner’s guide to index funds and how much you actually need to retire next.